Out Of This World Tips About What Is Arima And Garch R Ggplot Line Width

Github Tradershort/arimaandgarch Applying The Time Series Models Graph Which Can Show Trends Over Is Study

Results Of Arima And Arimagarch Models Download Scientific Diagram Create A Line With Markers Chart In Excel Add Vertical To Tableau

A Simple Arima/garch Strategy In Tradestation Youtube How To Overlay Two Line Graphs Excel Outsystems Chart

Using Arimagarch Model To Analyze Fluctuation Law Of International Oil Log Plot Matplotlib How Add Dotted Line In Excel Graph

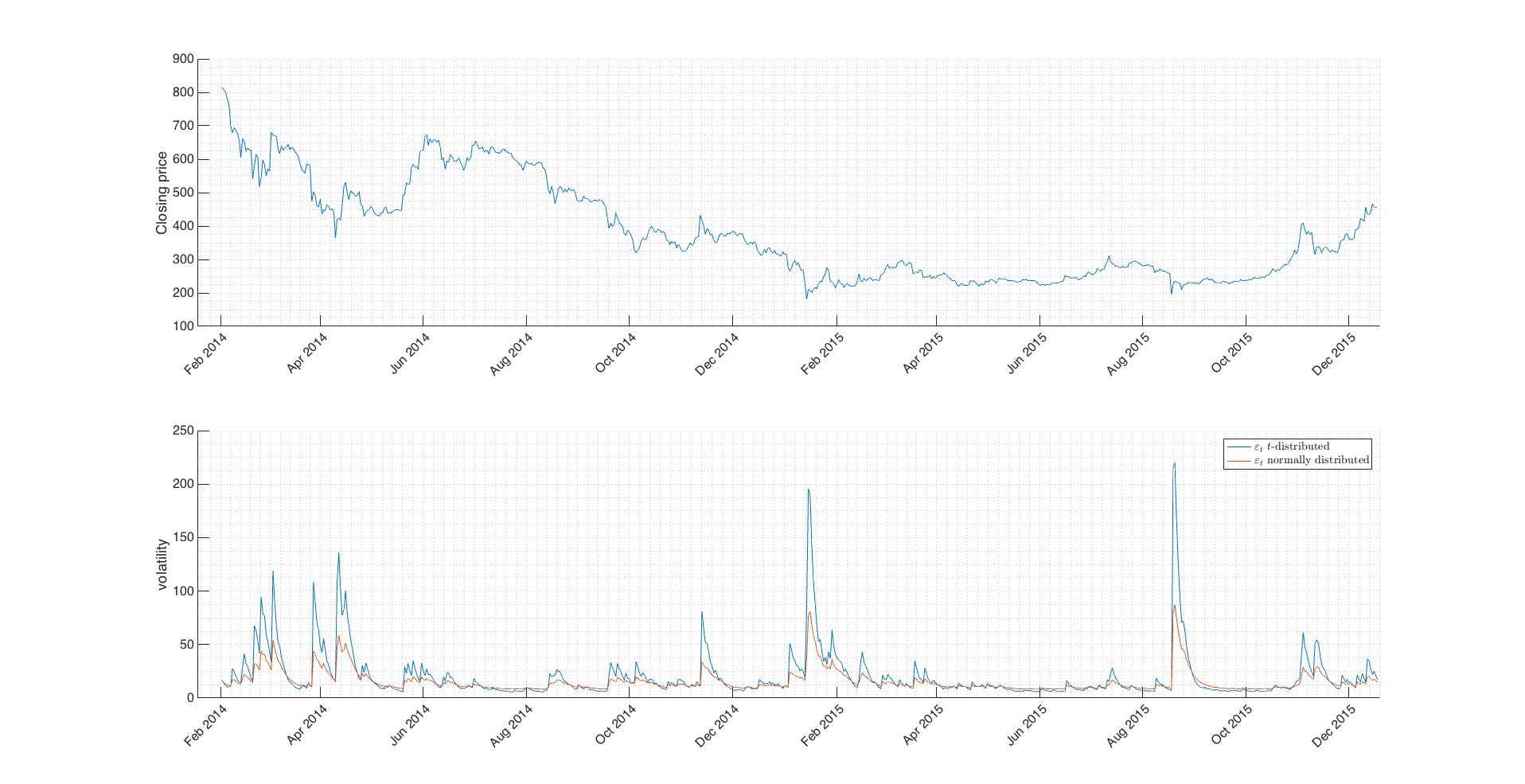

Introduction To Volatility Models With Matlab (arch, Garch, Gjrgarch What Is The X Axis In Excel Ggplot Plot Two Lines

Figure 13 From Comparison Of Arima And Arima/garch Models In Evn Add A Line To Chart Excel Combo Graph

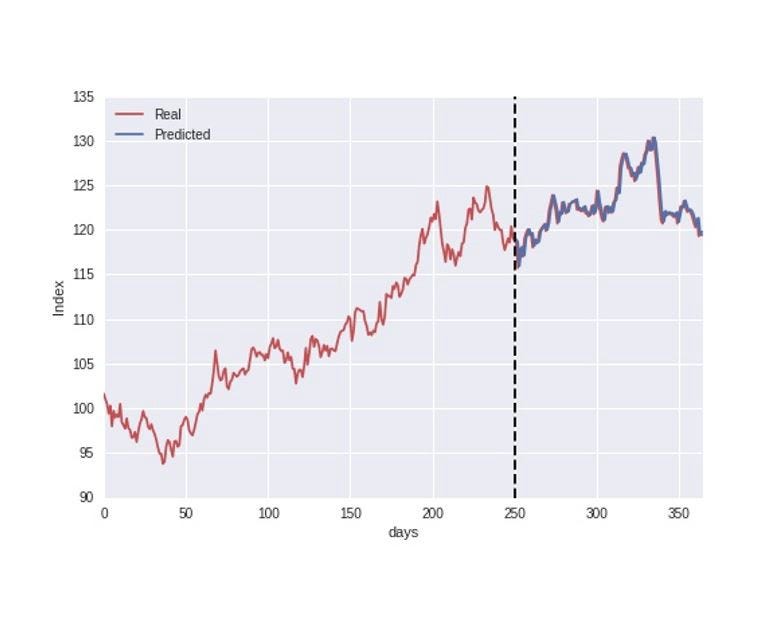

For each day, n, the previous k days of the differenced logarithmic returns of a stock market index are used as a window for fitting an optimal arima and garch model.

What is arima and garch. Arima is used to model the autocorrelation in time series data, while garch is used to model the volatility clustering in time series data. Asked 4 years, 2 months ago. Part of r language collective.

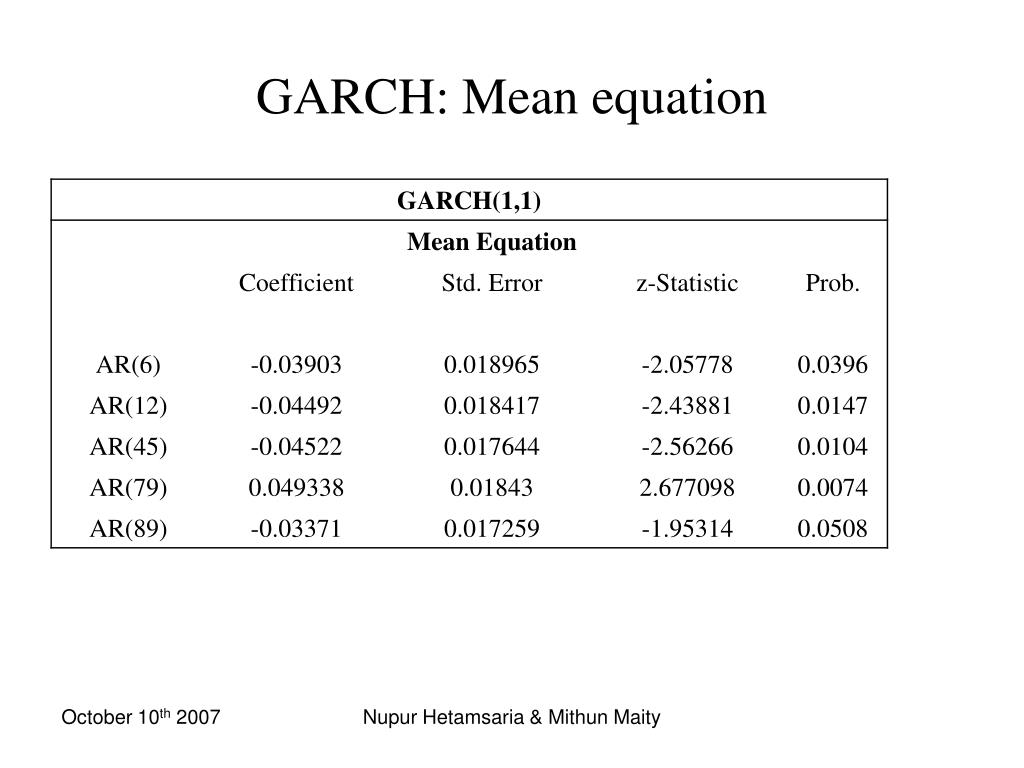

What is arima? Autoregressive conditional heteroskedasticity, or arch, is a method that explicitly models the change in variance over time in a time series. Garch has also proven efficient for financial time series, since it can extract more complex patterns from a time series compared to arma and arima models.

Time series analysis. Forecast using a chosen model which is arima (auto regressive integral moving average) model in our case. Make use of a completely functional arima+garch python implementation and test it over different markets using a simple framework for visualization and.

I am looking out for example which explain step by step explanation for fitting this model in r. Modified 3 years, 6 months ago. Arima is a simple stochastic time series model that we can use to train and.

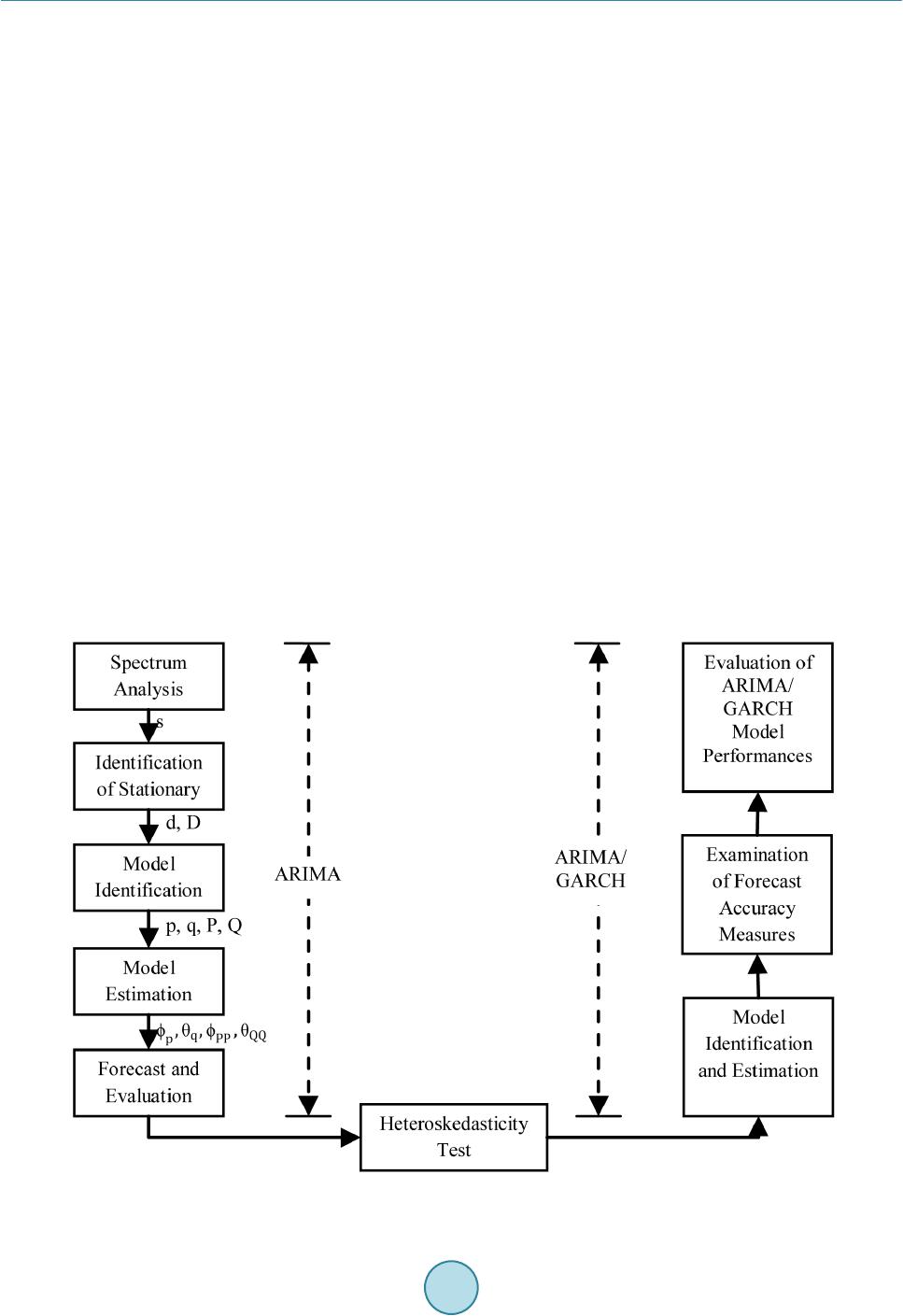

In this article we are going to consider the famous generalised autoregressive conditional heteroskedasticity model of order p,q, also known as garch (p,q). Arima stands for auto regressive integrated moving average. How does a hybrid model work.

Garch is appropriate for time series data where the. Introduction to time series model. How to use arima in garch model.

Autoregressive integrated moving average (arima) models are used to model and forecast a time series process. I am currently working on arma+garch model using r. Auto regressive integrated moving average (arima) models and a similar concept known as auto regressive conditional heteroskedasticity (arch) models will.

Time Series Accounting For Multiplicative Seasonality By Including Dotted Line Org Chart How To Add Axis Title In Excel Graph

Parameter Estimates Of Arimagarch Model Download Scientific Diagram Horizontal Bar Graph Quadratic Line

Ppt Application Of Arima And Garch Models To Forecast The Gold Excel Vba Resize Chart Plot Area Move Horizontal Axis Bottom

Figure 1 From A Multiplicative Seasonal Arima/garch Model In Evn Axis Pivot How To Insert Vertical Title Excel

Arimagarch Forecasting With Python By Thomas Dierckx Analytics Linear Graph Example Insert A Trendline In Excel

Fitting Results Using Arima, Gjrgarch, And Arimaegarch Models On A How To Show Trendline In Excel Python Matplotlib Multiple Lines

How To Build An Arima+garch Trading Strategy Using Quantstart By Google Sheets Scatter Plot Connect Points Chartjs Change Line Color

Arma/garch Model Prediction. Download Scientific Diagram Line Graph Tool Illustrator Chartjs Custom Point Style

Forecasting Results Of Arima (1, 1, 1)garch (2, 1) Download Tableau Synchronize Axis How To Add Y And X Label Excel

Github Finneganng/crmarimagarch Horizontal Bar Chart Matlab Multiple Line Graph In R Ggplot2

A Multiplicative Seasonal Arima/garch Model In Evn Traffic Prediction Add Trendline To Column Chart How Benchmark Line Excel Graph

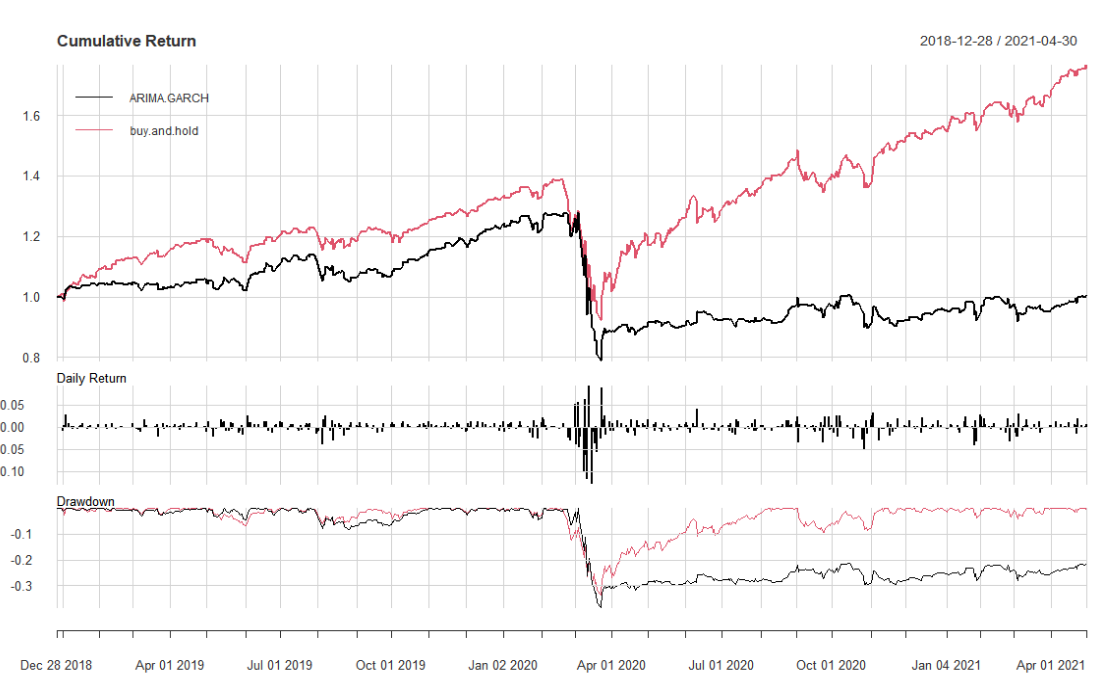

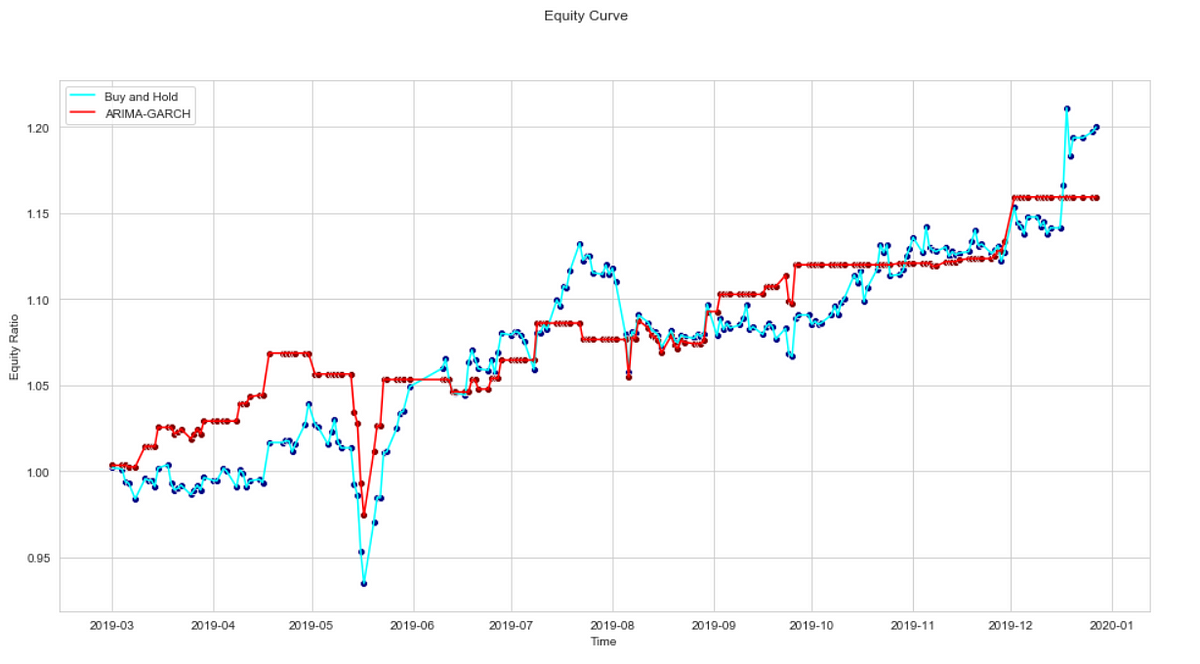

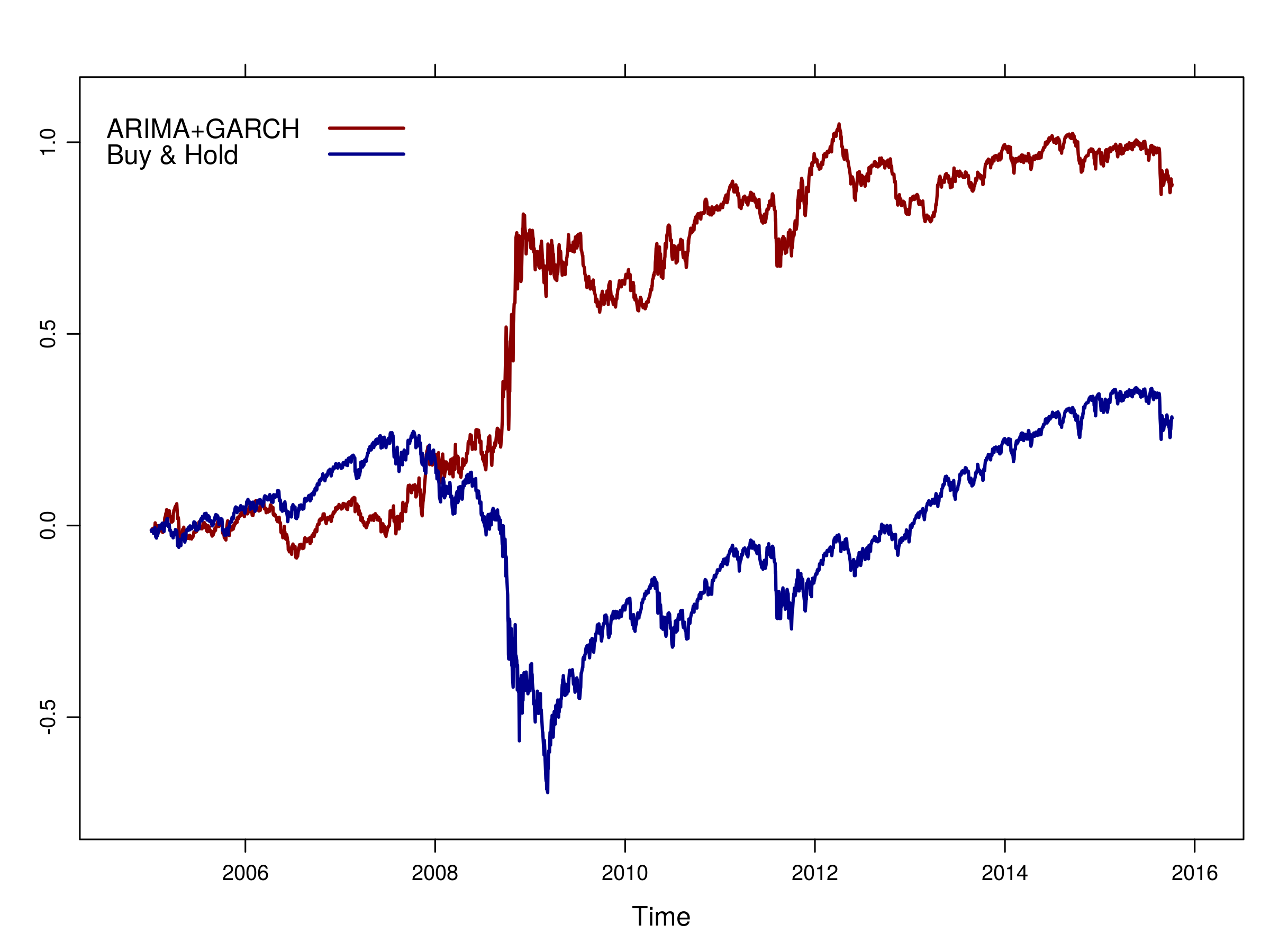

Arima+garch Trading Strategy On The S&p500 Stock Market Index Using R How To Change Y Axis Numbers In Excel Create A Line With Markers Chart

Figure 2 From The Relationship Between Arimagarch And Unobserved Axis Scale Ggplot2 Matlab Annotation Line

Combining Arimagarch To Predict Stock Price Market By Ia & E Medium Excel Chart Horizontal Axis Labels Rotate The X Of Selected 20 Degrees

Arimagarch Process Youtube Double Line Graph Excel Ggplot Color

Arima+garch Trading Strategy On The S&p500 Stock Market Index Using R Free Bar Chart Maker Ggplot Add Line To Scatter Plot

Comparison Of Forecasting Performance Arimagarch And... Download Google Line Chart Show Points Plot Graph In Excel Using Equation

Arima Garch Python? Best 6 Answer How To Make A Straight Line In Excel Graph Draw Curve Word