Simple Info About What Is The Formula For Simple Smoothing Time Series Line Plot Python

How To Leverage The Exponential Smoothing Formula For Forecasting Regression Line Ggplot2 Qlik Sense Combo Chart Reference

Ppt Chapter 7 Demand Forecasting In A Supply Chain Powerpoint Excel Chart Change Scale Double Broken Line Graph

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Line Chart Example Js D3 Stacked Area Tooltip

Solved Using Simple Exponential Smoothing And The Following Excel Draw Vertical Line On Chart Js Height

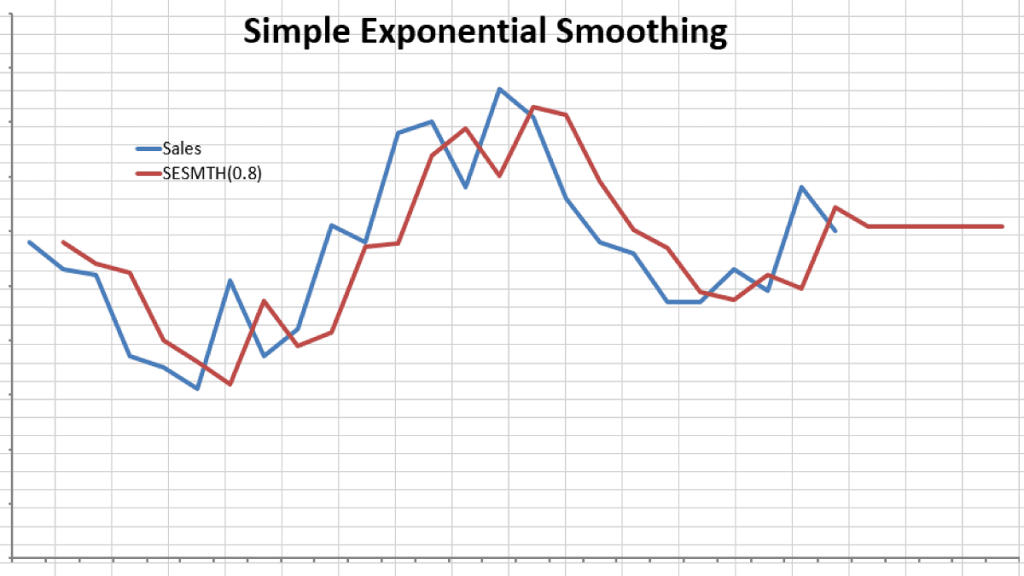

Simple Exponential Smoothing Youtube Combo Charts In Google Sheets Qlik Sense Chart Stacked Bar

Exponential Smoothing, Moving Average And Simple Youtube Line Char Matlab Plot

Y ^ t = α ( y t + ∑ i = 1 r ( 1 − α) i y t − i), where y ^ t is the forecasted value of the series at time t and α is the smoothing constant.

What is the formula for simple smoothing. Want something in between that weights most recent data more highly. ˆyt+1|t = αyt + α(1 − α)yt−1 + α(1 − α)2yt−2 + · · ·. Simple exponential smoothing is a simple — yet powerful — method to forecast a time series.

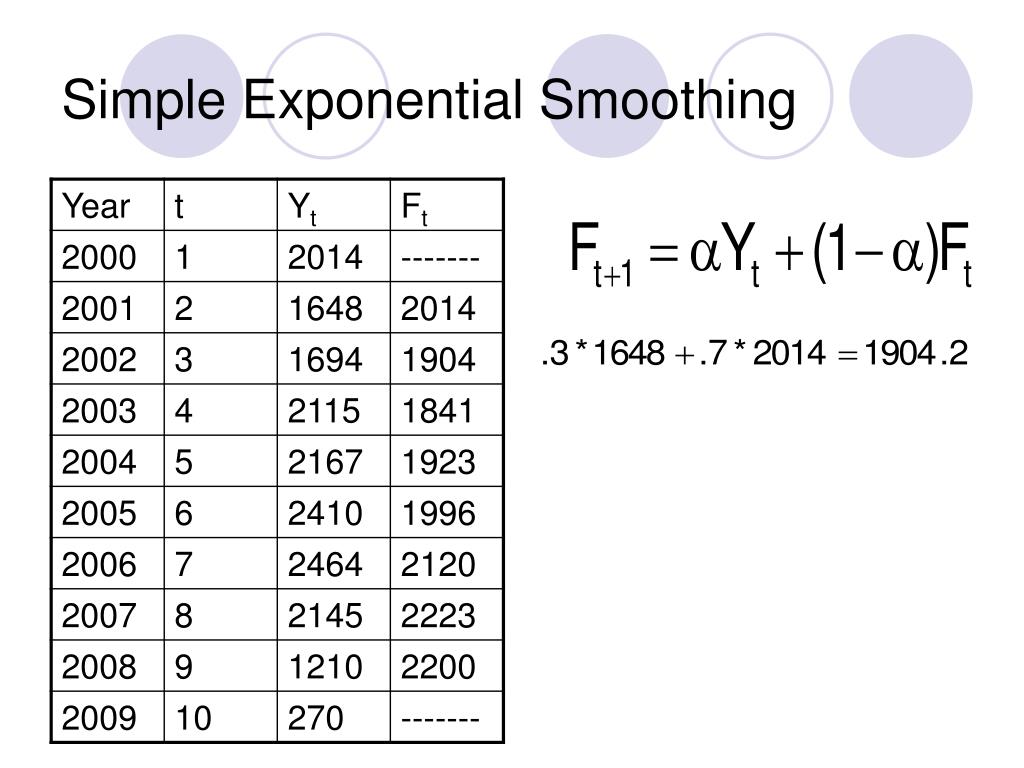

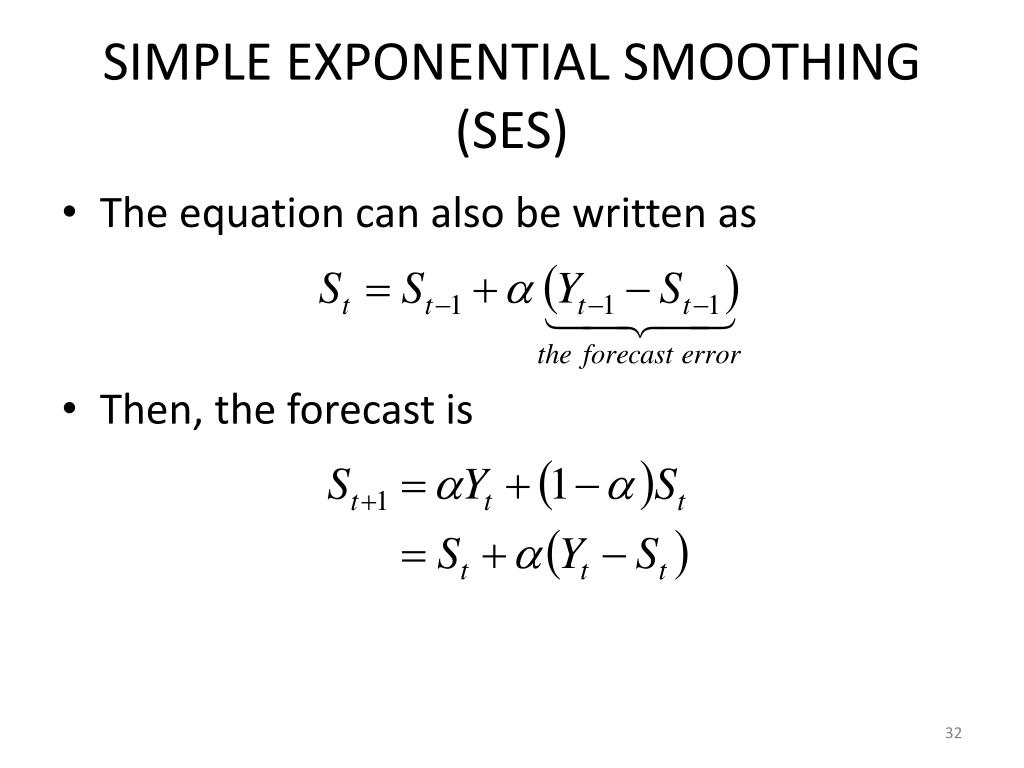

In other words, the smoothed statistic is a simple weighted average of the current observation and the previous smoothed statistic. What is simple exponential smoothing? The formula for simple exponential smoothing (ses) is:

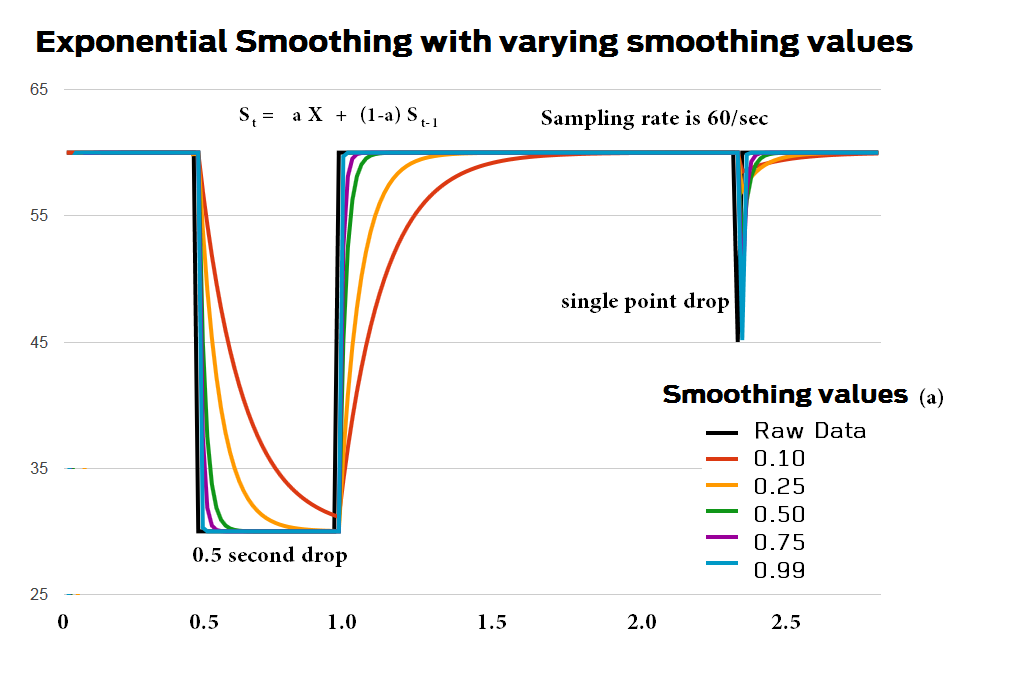

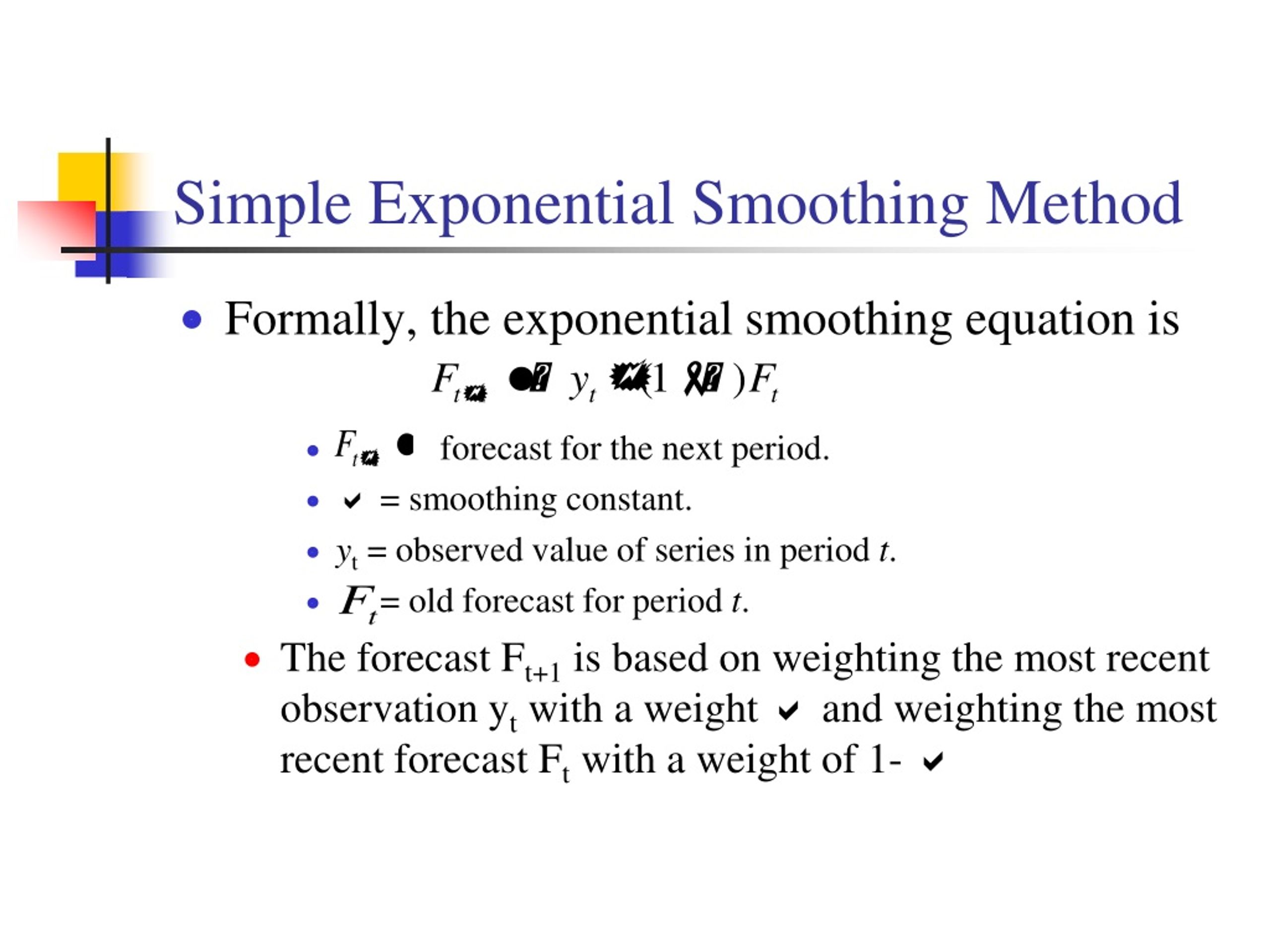

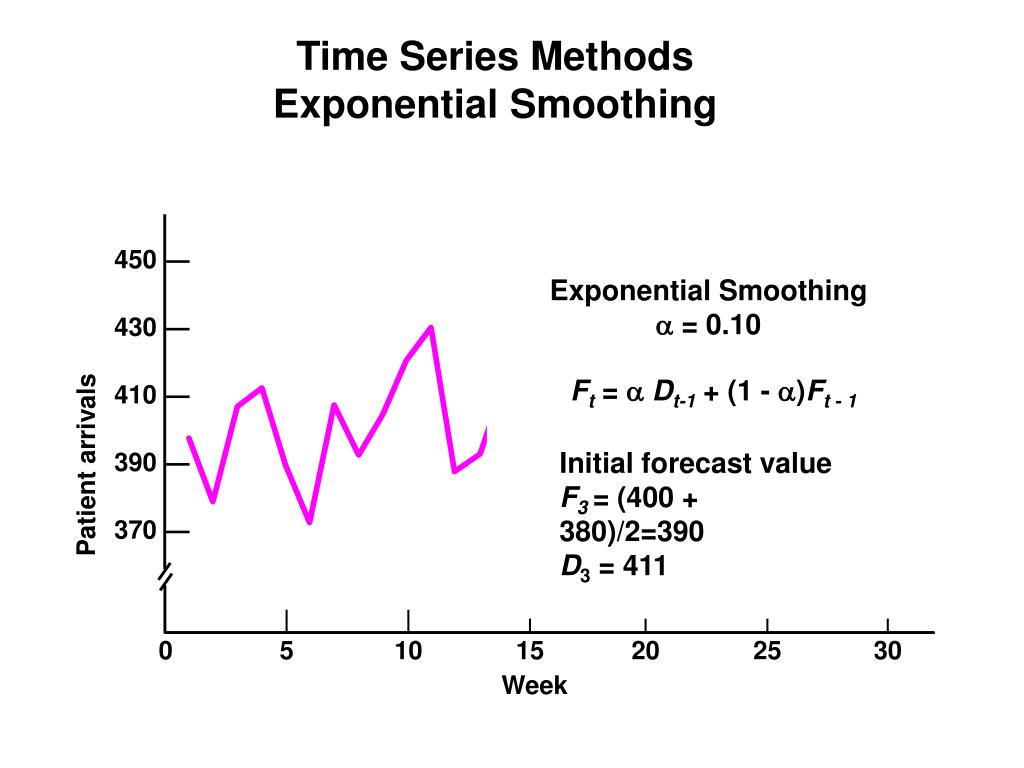

Simple exponential smoothing uses a weighted moving average with weights that decrease exponentially. F(t+1)= forecast for the next period f(t) = forecast for the most recent period a = smoothing constant (1 ò a ò 0) y(t) = actual value. Exponential smoothing in excel:

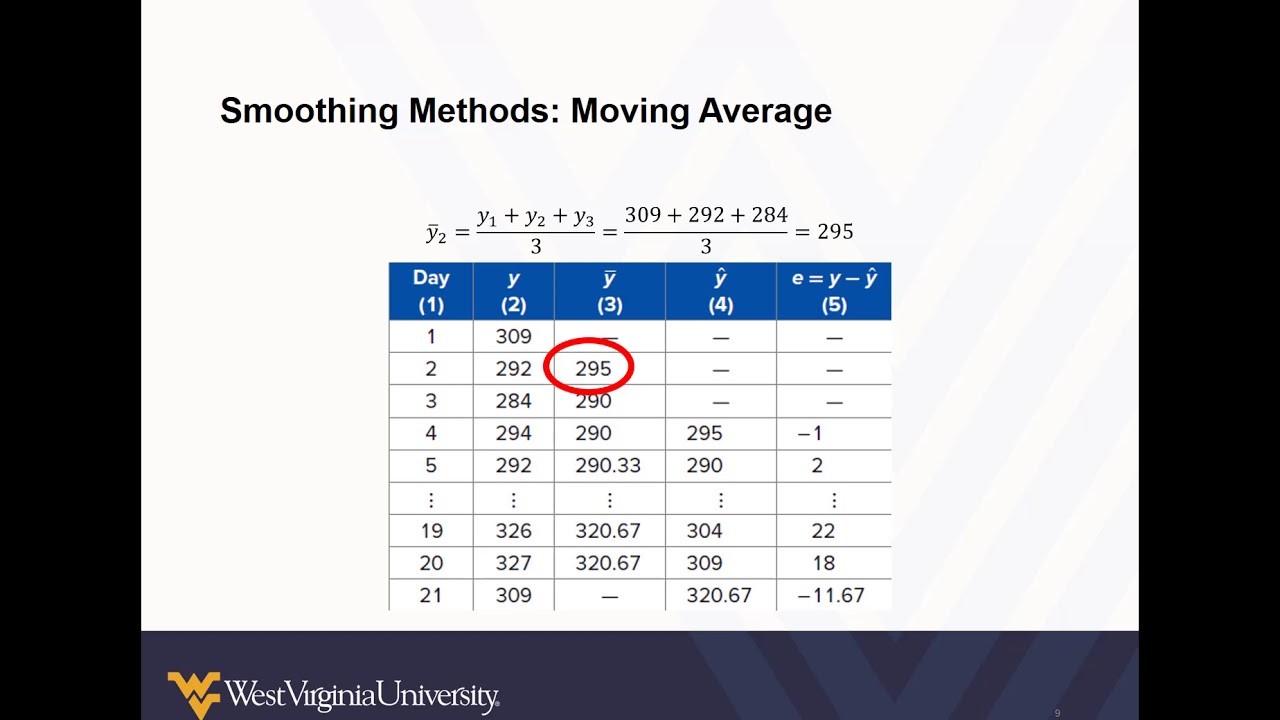

This method replaces each point in the signal with the average of m adjacent points, where m is a positive integer called the smooth width. Simple exponential smoothing is a time series forecasting method that assigns exponentially decreasing weights to past observations. The smoothing equation for the level (usually referred to as the level equation) gives the estimated level of the series at each period \(t\).

Where is the smoothing factor, and. Α is the smoothing parameter between 0 and 1. The equation for this method is:

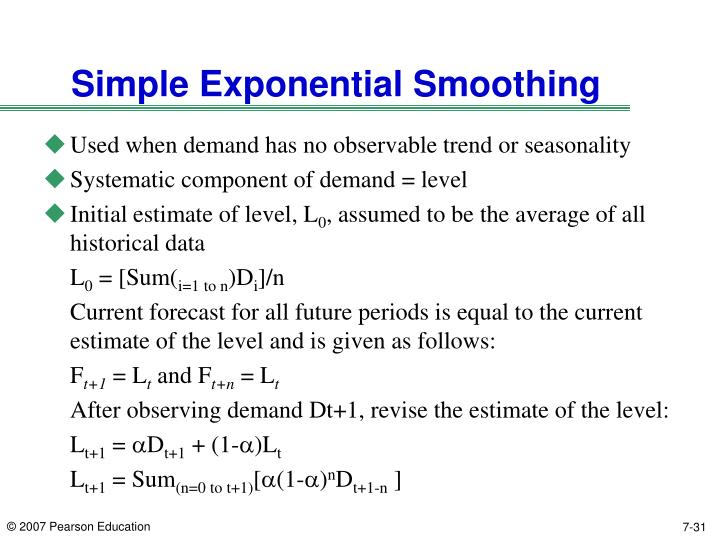

Following this, the best value for α is the one that results in the smallest mean squared error (mse). The forecast equation shows that the forecast value at time \(t+1\) is the estimated level at time \(t\). The forecast equation shows that the forecast value at time \(t+1\) is the estimated level at time \(t\).

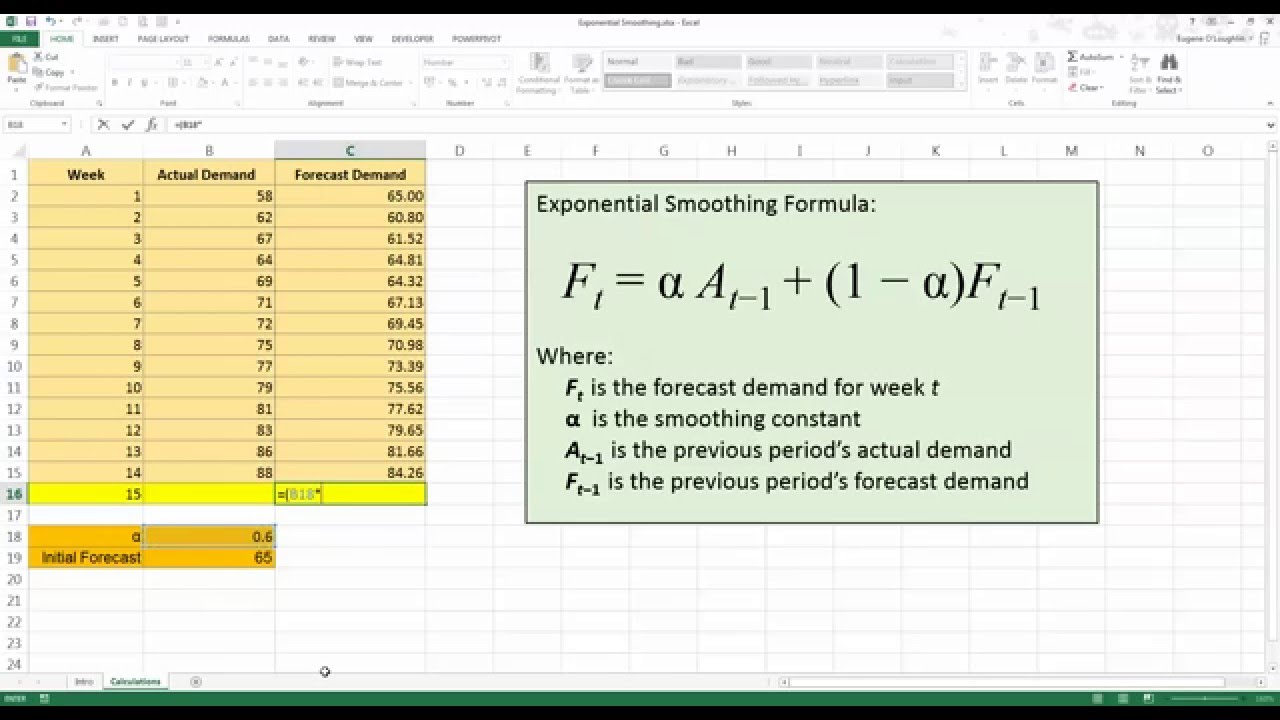

Exponential smoothing formula. Ft+1 is the forecast for the next period. The formula is mentioned below.

Single exponential smoothing smoothes the data when no trend or seasonal components are present. We normally use single exponential smoothing. Α = smoothing factor of data;

The formula for determining the forecast by the method of simple exponential smoothing is: Α α s t = α × y t + ( 1 − α) × s t − 1. Applying the forecast equation for time \(t\) gives \(\hat{y}_{t+1|t} = \ell_{t}\), the most recent estimated level.

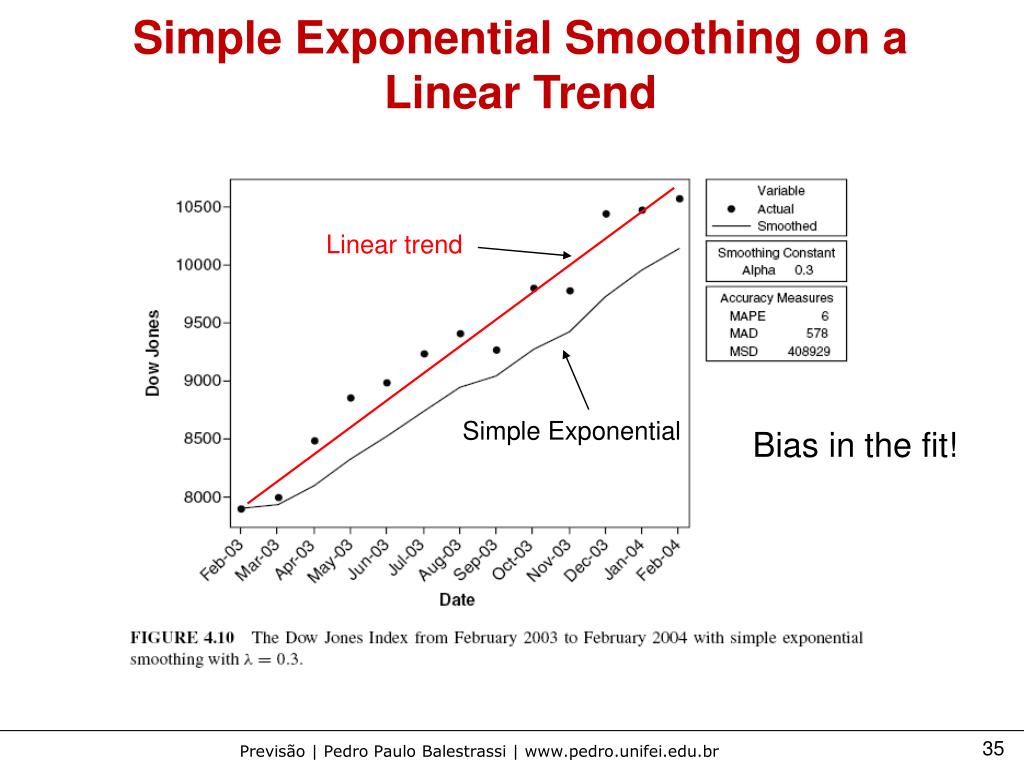

It was first formulated by brown and can be written as: The simple exponential smoothing model can be generalized to obtain a linear exponential smoothing (les) model that computes local estimates of both level and trend.

Simple Exponential Smoothing Complete Download Scientific Diagram Production Possibilities Curve Excel X Horizontal Y Vertical

Exponential Smoothing Method In Forecasting Techniques Switching X And Y Axis Excel Add Trendline To Chart

Ppt Section 7.2 Exponential Smoothing Powerpoint Presentation, Free Fit Curve Excel Ggplot Axis

Ppt 4 Exponential Smoothing Methods Powerpoint Presentation, Free Splunk Time Series Chart Combo Excel 2007

Simple Smoothing Methods Moving Average Youtube R Ggplot Plot Multiple Lines Add Line On Excel Graph

Moving Averages Smoothing Out The Noise For Better Predictions Ggplot Multiple Lines In R Line Plot Using Seaborn

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Dual Axis Chart Power Bi Excel Add Label

Ppt Exponential Smoothing Methods Powerpoint Presentation, Free Rotate Data Labels Excel Ggplot Several Lines

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Animated Line Chart D3 How To Create Graph In Excel With Two Y Axis

Ppt Stat 497 Lecture Notes 7 Powerpoint Presentation, Free Download Add Multiple Axis To Excel Graph Benchmark Line

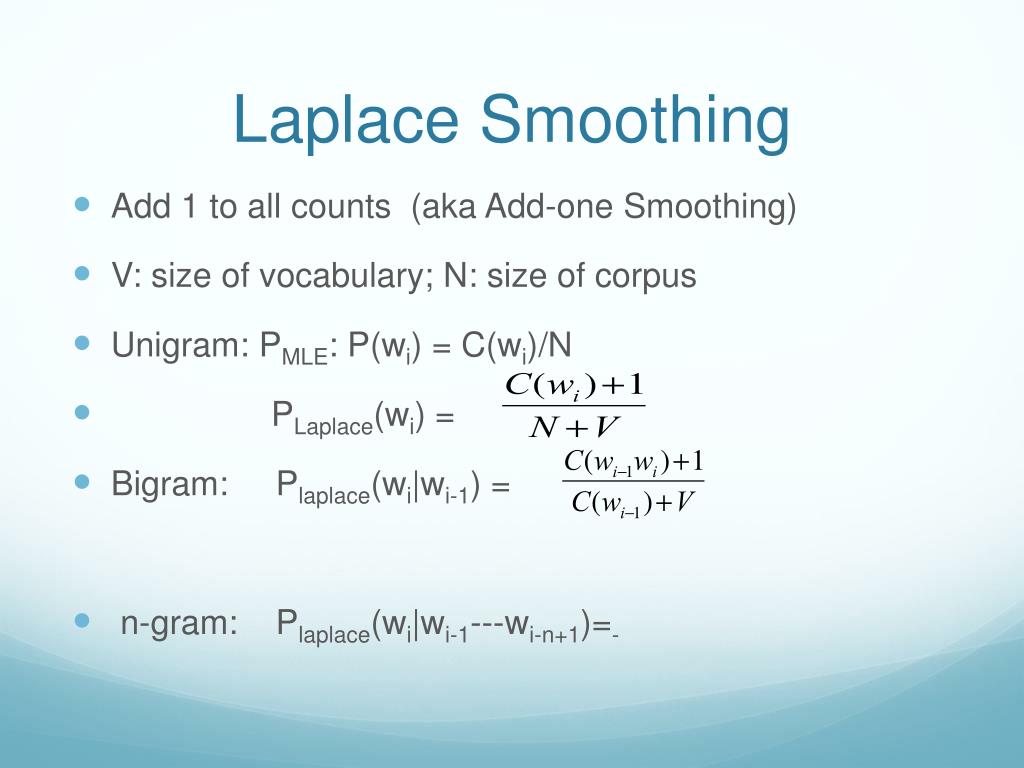

Ppt Smoothing Ngram Language Models Powerpoint Presentation, Free Reference Line In Power Bi Excel Plot X Vs Y

Simple Exponential Smoothing, Explained Directx Blogdirectx Blog How To Change The Axis In Excel Graph Sparkline Horizontal Bar

Exponential Smoothing Simple (part 2) Youtube How Do You Change The X Axis Values In Excel Matplotlib Draw Multiple Lines

Ppt Movingaveragemethods Powerpoint Presentation, Free Download Axes Of Symmetry Formula How To Edit Line Chart In Google Docs

Simple Exponential Smoothing For Time Series Forecasting By Nicolas Excel Combo Stacked And Clustered Charts Together Gnuplot Bar Chart Multiple

Archives For Simple Smoothing Numxl Reference Line Chart How To Construct A Graph In Excel

Ppt Outline Simple Moving Average Weighted Exponential How To Make Line Graph Using Excel In X And Y Axis

Ppt Stat 497 Lecture Notes 7 Powerpoint Presentation, Free Download Trendline On A Graph Solid Line Border Chart Excel