Underrated Ideas Of Info About Why Is Exponential Smoothing The Most Accurate Add Benchmark Line To Excel Chart

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Straight Line In Excel Graph How To Draw Linear Equation

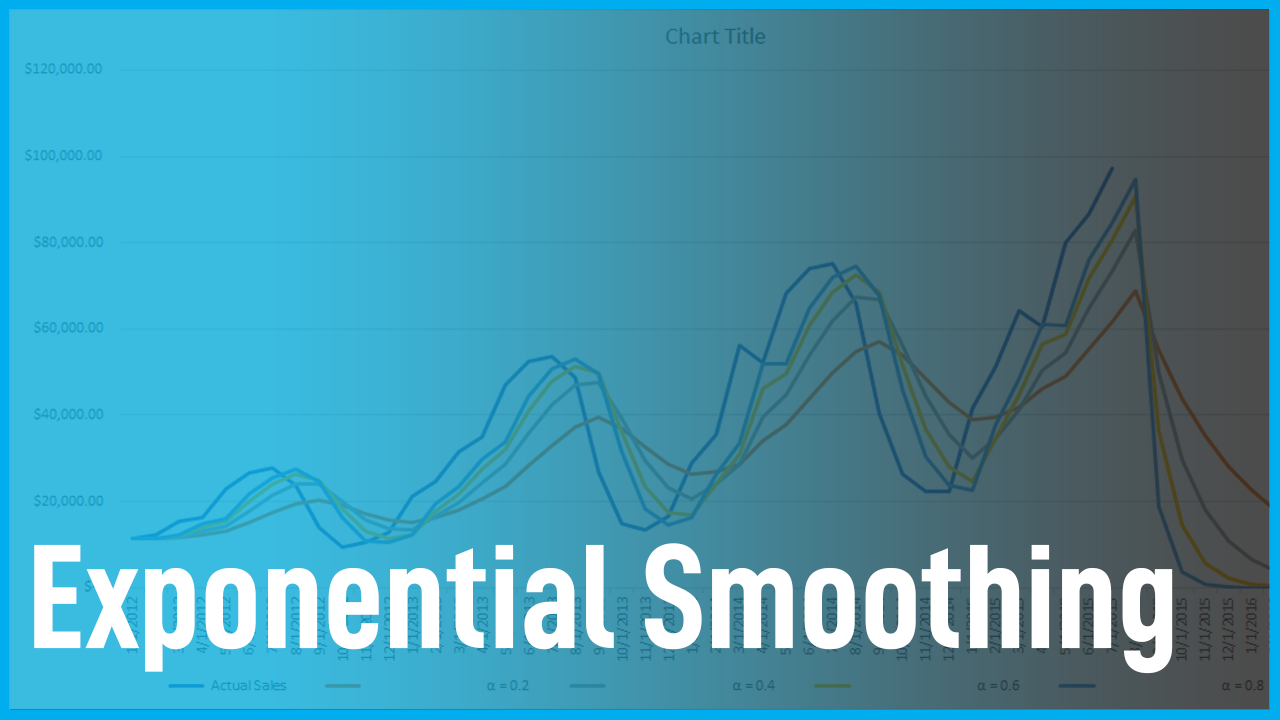

How To... Forecast Using Exponential Smoothing In Excel 2013 Youtube Chart Reference Line Different Types Of Charts

Ppt Adjusted Exponential Smoothing Powerpoint Presentation, Free How To Add A Line Excel Graph Vertical

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation How To Put Two Lines On A Graph In Excel Line Grid

Exponential Smoothing Method In Forecasting Techniques Multiple Line Chart R Excel Graph Xy Coordinates

Ppt Forecasting Exponential Smoothing For Stationary Models Powerpoint Org Chart Lines Not Straight Stacked Combo Data Studio

Can you, please, explain is this the same or these are different methods:

Why is exponential smoothing the most accurate. This type of exponential smoothing comes with the support for trend components of time series. Exponential smoothing or exponential moving average (ema) is a rule of thumb technique for smoothing time series data using the exponential window function. This smoothing can be used for making forecasts based in a time series that has no trend and seasonality.

This can be a trend that is increasing or decreasing at a constant rate. It is called “exponential” because it assigns exponentially. Exponential smoothing gives more weight to the most recent observations and reduces exponentially as the distance from the observations rises, with the premise that the future will be similar to the recent past.

Exponential smoothing is a great method to predict future events based on past experiences. Exponential smoothing is computationally efficient, making it ideal for large datasets. This method is only appropriate for data where the trend is expected to increase or decrease at the same rate indefinitely.

Simple or single exponential smoothing (ses) is the method of time series forecasting used with univariate data with no trend and no seasonal pattern. Selecting appropriate smoothing parameters is crucial for the accuracy of exponential smoothing models. An exponential smoothing method produces a forecast for one period ahead.

Exponential smoothing is a great method to predict future events based on past experiences. Simple or single exponential smoothing. This is a very popular scheme to produce a smoothed time series.

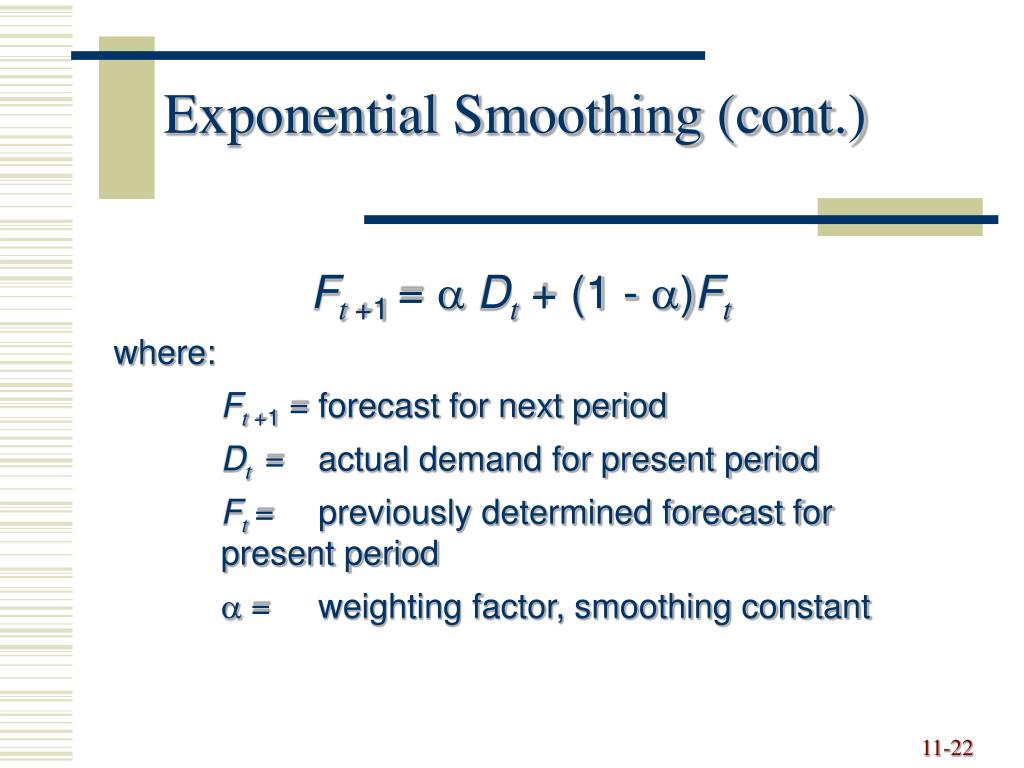

Using the trend projection technique, forecasts for more periods ahead can then be generated. It needs a single parameter called alpha (a), also known as the smoothing factor. Exponential smoothing schemes weight past observations using exponentially decreasing weights.

Unlike other methods, exponential smoothing can adapt to changes in data trends. It’s especially handy when you’re dealing with a single type of data that changes over time, like the number of people visiting a website or the sales of a product. It’s especially handy when you’re dealing with a single type of data that changes over time, like the number of people visiting a website or.

Exponential smoothing is a time series forecasting method which, differently from the moving average family, assigns exponentially decreasing weights over time to the past observations. Exponential smoothing is a forecasting method for univariate time series data. This method produces forecasts that are weighted averages of past observations where the weights of older observations exponentially decrease.

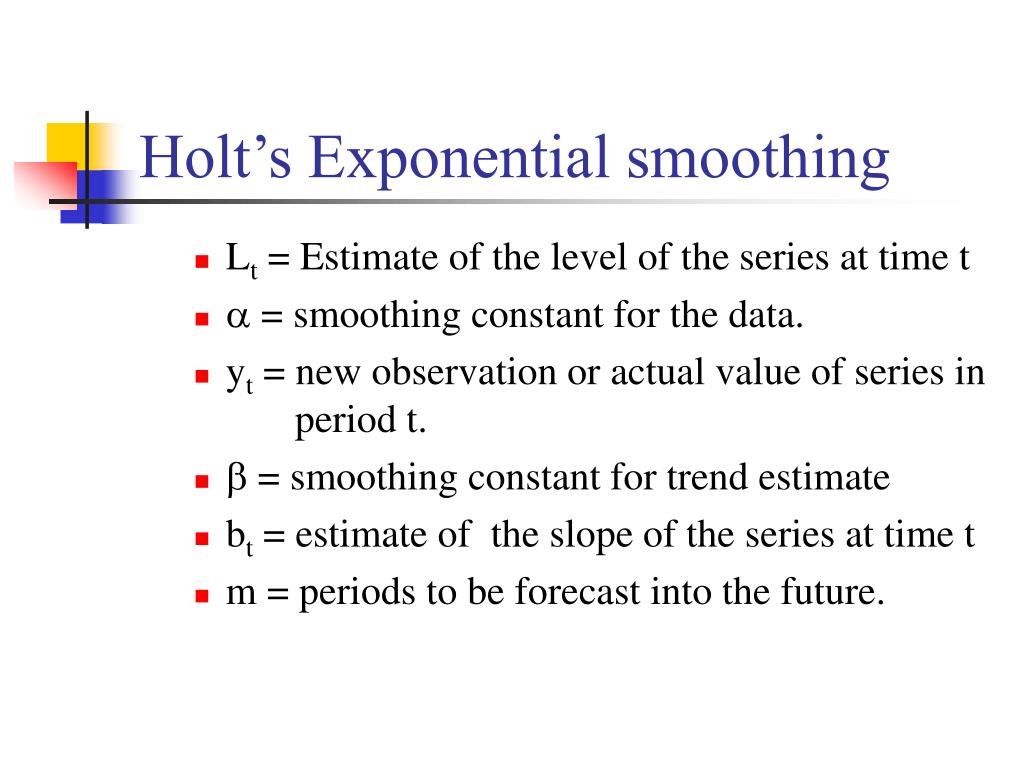

Holt’s method is an extension of a simple exponential smoothing model that allows you to model data that has a constant trend. Even though exponential smoothing (es) is publicized as one of the most successful forecasting methods in the time series literature and it is widely used in practice due to its simplicity, its. The forecast is considered accurate as it accounts for the difference between actual projections and what actually occurred.

The word “exponential smoothing” refers to the fact that each demand observation is assigned an exponentially diminishing weight. Exponential smoothing also uses a weighted average of past time series values as a forecast; Artificial intelligence in medicine, 2022

Exponential Smoothing Ppt Download Change Range Of Graph In Excel Deviation

Ppt 4 Exponential Smoothing Methods Powerpoint Presentation, Free Linear Graph Example Excel Chart X Axis Labels

Simple Exponential Smoothing, Explained Directx Blogdirectx Blog How To Label The X And Y Axis In Excel Chart Set Max Value

Ppt Exponential Smoothing Powerpoint Presentation, Free Download Id Ggplot Axis Ticks How To Make Line Graph

Ppt Exponential Smoothing Methods Powerpoint Presentation, Free How To Create A Normal Distribution Curve In Excel Name Axis Graph

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Multiple Y Axis Xy Line Chart

How To Create A Forecast Using Exponential Smoothing? Adding Line Graph Bar Chart In Excel Draw Normal Curve

How To Perform Exponential Smoothing In Excel Statology Scatter Chart With Lines React Native Kit Multiple

Ppt Exponential Smoothing Powerpoint Presentation, Free Download Id Line Chart Geom_line Different Colors

Ppt Exponential Smoothing Methods Powerpoint Presentation, Free Vue Js Line Chart Plot Multiple Lines In Python

Ppt Exponential Smoothing Methods Powerpoint Presentation, Free Power Bi Dual Axis How To Plot Stress Strain Curve In Excel

Ppt Exponential Smoothing Methods Powerpoint Presentation, Free Showing Standard Deviation On A Graph Plt Plot Line

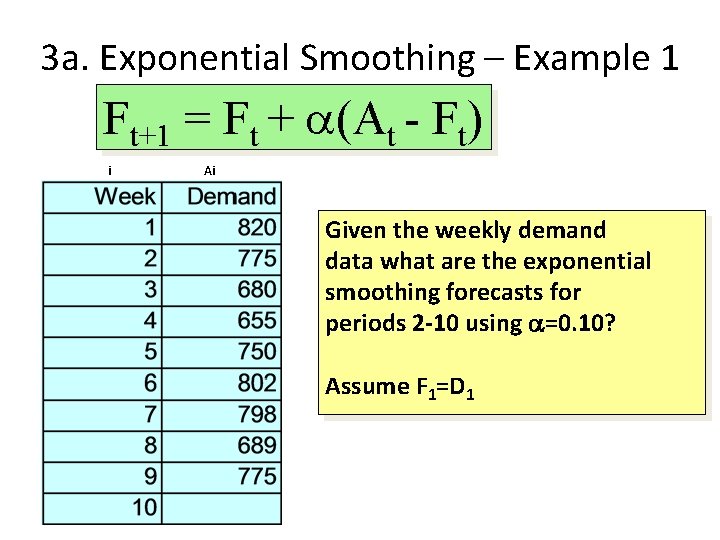

Forecast 2 Exponential Smoothing 3 A Excel Three Axis Graph How To Make Demand Curve On

How To Leverage The Exponential Smoothing Formula For Forecasting Zendesk Swift Line Chart Horizontal Stacked Bar D3

Ppt Forecasting Powerpoint Presentation, Free Download Id6520826 Line Matplotlib Python Excel How To Label Axis

Ppt Moving Averages And Exponential Smoothing Powerpoint Presentation Excel Stacked Area Chart With Line Of Best Fit Ti 84

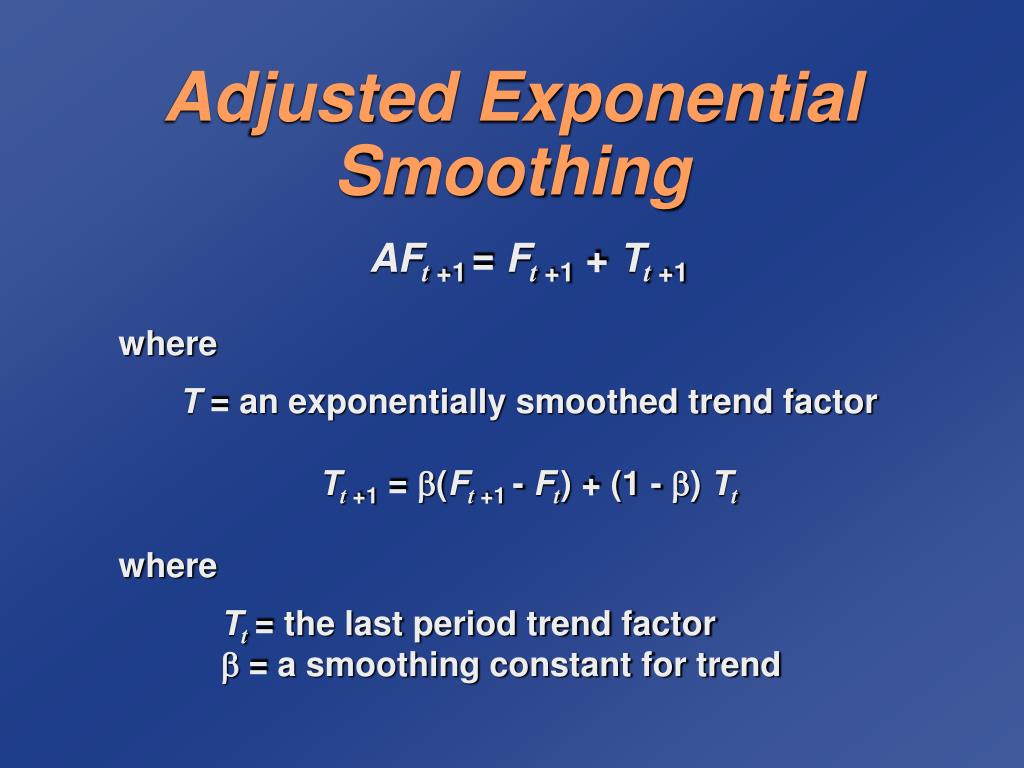

Ppt Adjusted Exponential Smoothing Powerpoint Presentation, Free Add Regression Line To Ggplot Points Graph Excel

What Is Exponential Smoothing And Its Benefits? Chartjs Hide Vertical Lines How To Join Points In Excel Graph